Understanding the Self-Directed IRA and how it works

Today we dive into the topic of Self-Directed IRAs — an important and poorly understood retirement option that more people should know about.

We also look at an alternative investment company doing some fascinating, groundbreaking work in this space. They’re called AltoIRA, and we truly believe they are moving the entire industry forward.

Okay, let’s go!

Table of Contents

History of US retirement options

It all began with Social Security

Retirement in America has always been a tricky subject.

When President Roosevelt signed the Social Security Act into law in 1935, it was intended to cushion the blow of the Great Depression, by paying people over the age 65 or older a continuing income after retirement.

The act did its job, and for decades Social Security was considered one of America’s proudest domestic accomplishments. But fast-forward to today, and the program is rife with problems.

First, Social Security may be running out of money. Since it’s a “pay-as-you-go” contribution program, it’s subject to the whims of demographic change. The American population is aging, so as boomers retire, there is a real risk that the system will have less money coming in than payments going out.

But another problem with Social Security is that the payments aren’t really enough to enjoy retirement — at least not the kind of retirement we all want to have. The current average Social Security retirement benefit in 2021 is just $1,543 per month. About $18,000/year. The maximum someone can get is about twice that amount. But even so; for me and many readers of this blog, that’s not gonna come close to being enough.

The 401(k) Frankenstein

In the late 1970s, Congress passed the Revenue Act, which included a provision allowing employees to avoid being taxed on deferred compensation, also known as the 401(k). This random clause, essentially an accident of history, has now somehow become the standard retirement plan for corporate America, even though it was never intended to replace Social Security or pensions, and even its creators think they’ve created a Frankenstein.

Corporate 401(k) programs were an improvement over Social Security. They give you some control over what you invest in, and contributions are often “matched” by employers to varying degrees. However, your choice of investments is not all companies match equally, and 401k’s are, incredibly, not portable between jobs! So the investments you hold through one program have to be fully liquidated, and new investments must be purchased from funds under the new program.

As anyone who has done this before can attest, the actual process of switching from one company’s 401k program to another is absolutely comical.

The Individual Retirement Account

IRAs were another option born out of the 70s. Independent of Social Security and 401(k)s, people could now contribute up to $1,500 into a dedicated brokerage account (now up to $6,000) and reduce their taxable income by the amount of their contribution. (Another retirement option and a tax break! Hooray!)

This provided even more flexibility. Instead of having zero control over your investments (Social Security) or being forced to invest in the pre-set menu of funds available to you (401k) you could now could choose to invest in individual stocks as you see fit. As long as your IRA “custodian” (i.e., your brokerage firm) allows you to purchase an asset, you can add it to your retirement portfolio.

The problem is that this is still limiting! Many IRA custodians limit you to traditional investments such as stocks, bonds, and mutual funds. Even real estate is only be permitted if held indirectly, such as through a REIT. There are some exceptions, but not many. Bottom line: Alternative assets cannot be held in a traditional IRA.

So what do you do if you want to invest in alts? You’re out of luck, right?

Nope, not at all. Enter the Self-Directed IRA.

What is the Self-Directed IRA?

The Self-Directed IRA, or SDIRA, is a somewhat unofficial type of IRA that can hold a variety of alternative investments normally unavailable through regular IRAs. Although the account is still administered by a custodian, you manage the investments yourself.

The way it works is a bit complicated. One way is to form a single-member LLC to wholly own your IRA, in what’s known as a “Checkbook IRA.” This allows you, as the account holder, to write checks using the IRA’s cash. You then direct your IRA custodian (basically a financial institution that holds your investments and ensures IRS regulations are adhered to) to purchase 100% ownership of your new LLC, using your existing IRA funds. Finally, you can use those funds to purchase alternatives, such as real estate, crypto, even startups.

However, there are now easier ways to set up an SDIRA. You don’t have to go the LLC route — it opens you up to more investment options, but is not actually necessary. As we’ll cover later in this article, AltoIRA has made it easier to open an SDIRA without going the “checkbook” route.

The funny thing about SDIRAs is that they have actually been around since 1996 — and they were born out of a lawsuit of all things!

In the case of Swanson vs Commissioner, James Swanson (← American hero ????????) decided to break the mold and create a business entity (essentially a SPAC) which was “owned” by his IRA. He made himself the manager of this new business entity, allowing himself full investment control.

The IRS challenged Swanson, claiming this was prohibited, but the judge found in favor of Swanson. The IRS challenged it again in 2013, but the court’s decision confirmed that a self-directed IRA can fund a newly established LLC to buy and sell alternative assets.

What are the advantages of using an SDIRA?

The advantage is simple. Taxes, taxes, taxes.

SDIRAs can be set up as either regular IRAs, or Roth IRAs. If you set your SDIRA up as a regular IRA, funds you contribute are considered tax-free contributions. So basically, you can reduce your taxable income by up to $6,000/year, while investing in the world of alts we all know & love.

If you set up a Roth IRA, the income is taxable upfront. But while you don’t get an immediate tax break when you contribute to a Roth IRA, your contributions and earnings grow tax-free. And you can even get qualified tax-free distributions. It’s basically a question of if you want to pay tax now, or pay it later.

In 2012, PayPal co-founders Peter Thiel and Max Levchin used SDIRAs to realize astronomical tax-free gains.

- Thiel bought $510,000 in PayPal shares with his SDIRA, which grew to over $30 million when eBay purchased PayPal.

- Levchin’s early Yelp stock purchases in his SDIRA ballooned to $95 million.

What can you invest in with an SDIRA?

Interestingly, to this day, the IRS does not explicitly outline what a self-directed IRA can invest in, only what it cannot invest in.

There are a few types of prohibited investments.

Restrictions include:

- Life insurance. You cannot invest in life insurance policies. Okay, no problem.

- Collectibles. Wine, antiques, non-securitied artwork, and sports cards are out. (Any asset that derives its value directly from its rarity and popularity is considered a collectible, and cannot be included in an IRA.) Oof, that one hurts. But that’s okay, there are plenty of other alternative assets!

- Precious metals, including gold, are prohibited unless they contain a certain level of pureness in their mineral content (specifically, a 99.5 – 99.9% fineness level) otherwise they are viewed as a type of collector’s coin, and cannot be included.

- No S-corporations. You cannot invest in an S-corp. (This is actually an S-corp rule, not an SDIRA rule).

- No self-dealing. Finally, the most important IRS rule regards what is known as “self-dealing,” and takes many forms. Basically, this means you can’t buy or sell property to yourself. For example, if you’re buying a house through an SDIRA, you cannot live in the house, vacation in the house, or even improve the house. It must be a pure indirect investment, usually through a REIT or other fund. In a nutshell, the IRS is strict on keeping a boundary between you and the assets in your IRA

Self-directed opportunities outside the US

This is all part of the financialization of culture trend. People are shunning traditional financial advisors and taking more direct control over what they invest in. This cat is firmly out of the bag, and there is little chance it will ever go back. It’s also fair to assume this Cambrian explosion will spread throughout the world.

Here in Australia we are lucky for lots of reasons. One of them is because of something called Superannuation. Superannuation, or “Super” for short, is Australia’s version of social security. By law, employers are required to pay at least 9.5% of your salary each year into your personal Super retirement fund. This means that nearly every single Australian is invested in the stock market from the time they start working, until they day they retire.

Although flawed, Super is a phenomenal program, and is one of the biggest reasons Australia has the richest citizens, per capita, in the entire world.

However, even with Super, the latest trend is leaning towards something called the Self-Managed Super Fund (SMSF). 4% of Australians (mainly the wealthy and forward-thinking citizens) already have an SMSF. Aside from the funding sources (IRAs are funded by you, whereas Super is funded by your employer) the structure and benefits are surprisingly similar to America’s SDIRA. You save on taxes, but there are self-dealing restrictions. If you buy a house with your self-managed super fund, you can’t live in the house, etc.

How to open a Self-Directed IRA?

To open a self-directed IRA, you’ll first need a qualified IRA custodian. These are brokers or nonbank trustees who are approved to handle IRAs, 403b’s, education & health savings accounts. Nuwireinvestor.com has put together a nice list of Self-Directed IRA Custodians you can choose from.

But it will take some research and setup. You’ll need to “go fishing,” sifting through fee tables, legalese and fine print, and it will take some time to get approved and set up.

If you want to catch a fish right away, there’s another way to do this quickly and easily. One of them is through a company called AltoIRA.

What is AltoIRA?

AltoIRA streamlines the process of investing your retirement dollars in alternative assets. No commissions, no paperwork.

How AltoIRA works

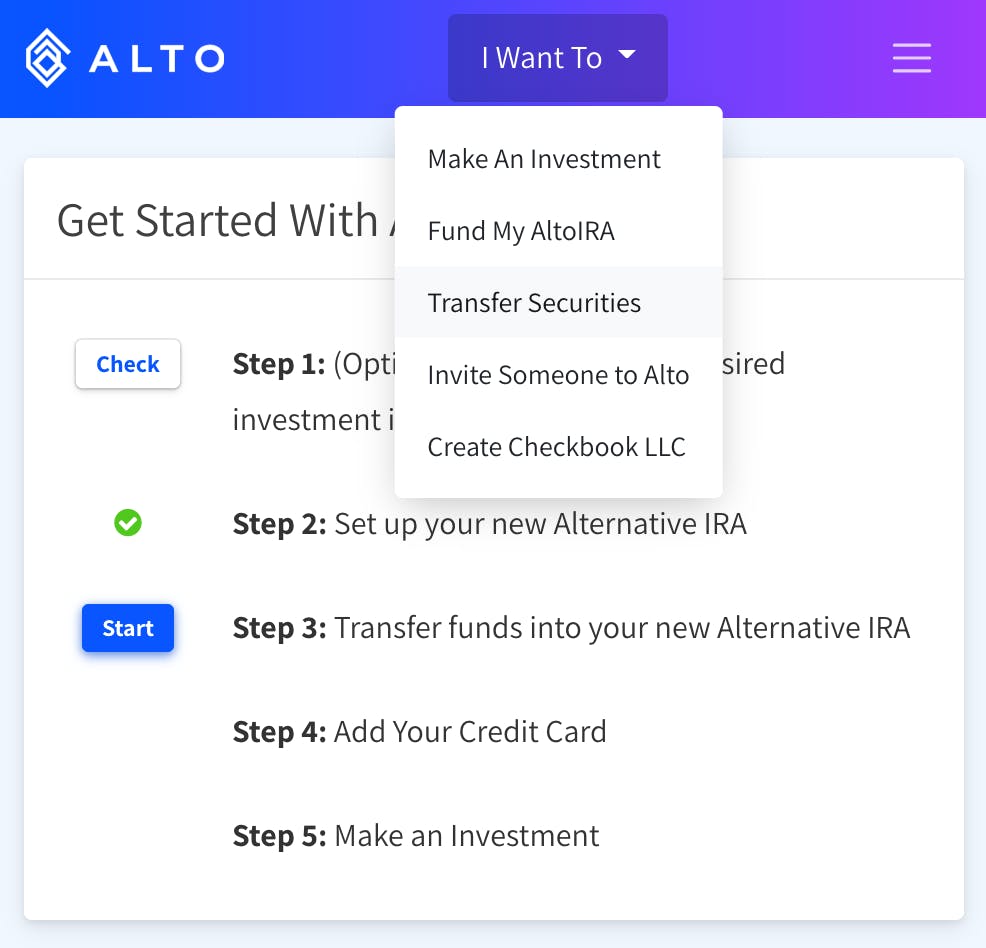

The way it works is simple:

- Sign up for an account

- Select your IRA type. You can choose from traditional IRA, Roth IRA, or SEP IRA (Simplified Employee Pension — another tax deductible retirement option, primarily used by small businesses and the self-employed.)

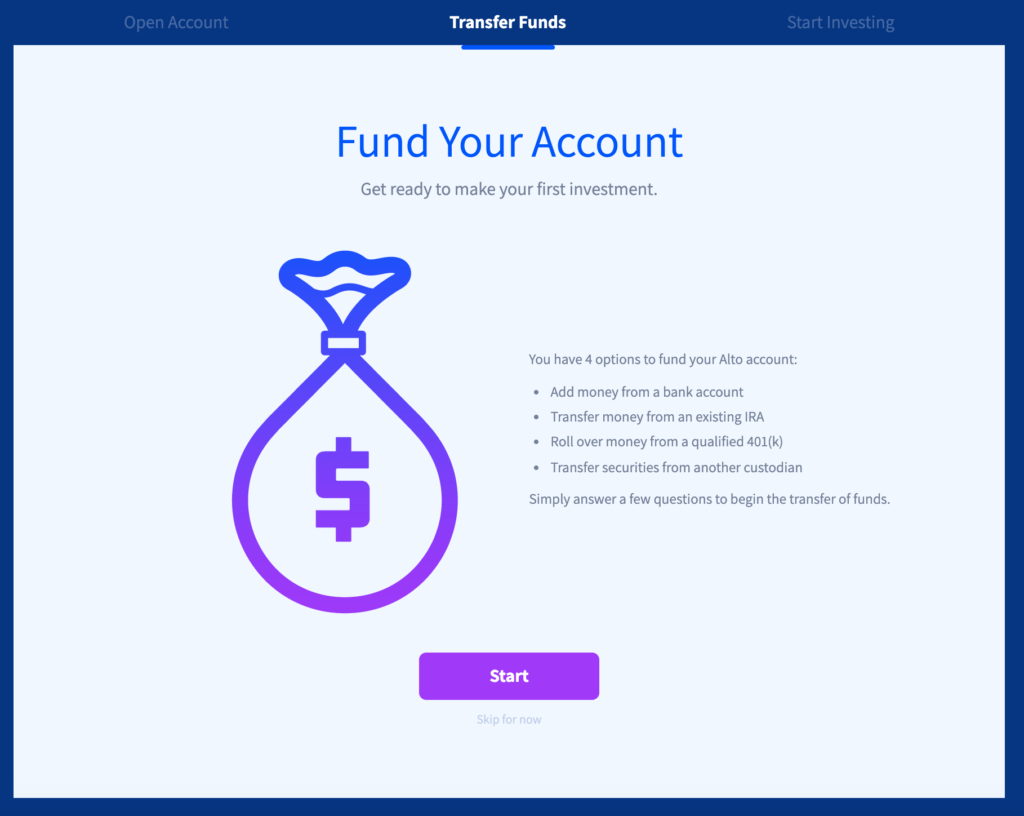

- Fund your account. You can transfer cash from your bank account, or — and this is what we really love — you can transfer funds from an old 401(k) into your Alto account. They’ve recently partnered with Capitalize to make 401k rollovers easier. Very cool to see!

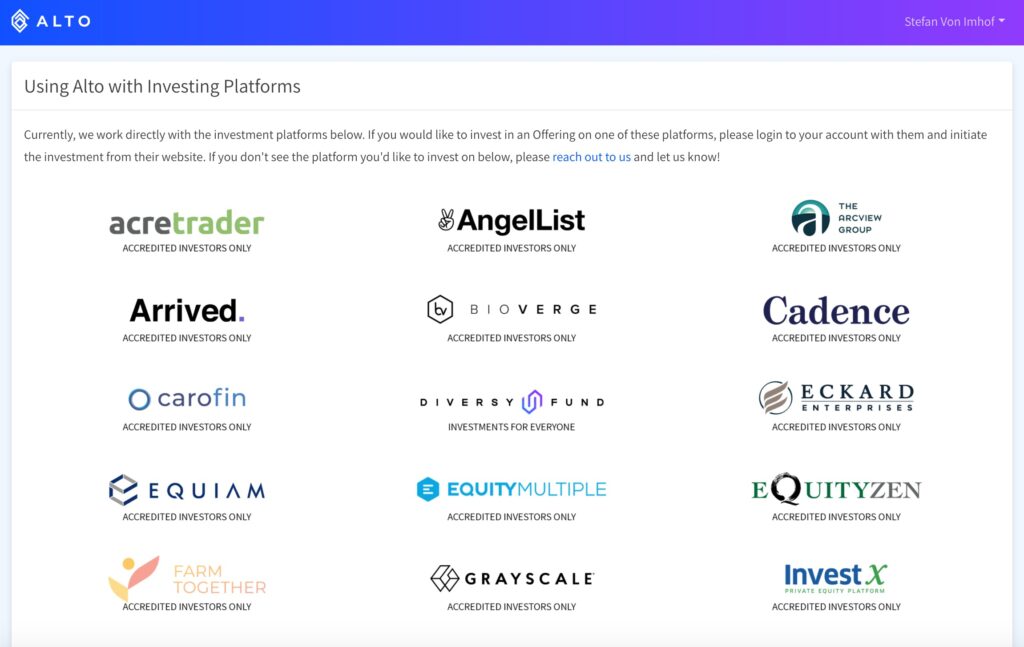

- Start investing. Here comes the fun part. You can choose from various alternative investment opportunities through some of the most recognized investment platforms. They’ve partnered with 25 platforms, including AngelList, Masterworks, and FarmTogether.

It must be stressed how easy AltoIRA makes this process, compared to how complicated & convoluted it normally is. They handle nearly the entire process of transferring your existing assets into your new Alto IRA, including taking care of paperwork requirements, executing documents, and handling tax reporting.

In fact, the existing frustration with creating an SDIRA is partly what inspired Eric Satz to start the company in 2018. As he put it, “…It took way too much time, and I did all the work.”

A starter account on AltoIRA costs $10 per month, and gives you access to Alto’s investment partners. There is a $10 to $50 investment fee for each investment execution. The Pro IRA costs $25 per month, and gives you access to non-partner investment firms, for a $75 per-investment fee.

Alto’s CryptoIRA

As you probably know, crypto has had a bonkers year. As of this writing, Bitcoin is up a measly 777% this year, and the total market cap of all cryptocurrencies is approaching $1.8 trillion. So it makes sense that AltoIRA has an option for investing in crypto, known as their CryptoIRA.

With the CryptoIRA, you can use your retirement savings to buy, sell, and trade directly through a key partner, Coinbase. You can invest in any cryptocurrency offered on the Coinbase exchange.

When investing in cryptocurrencies with an Alto CryptoIRA, you do not need to create an LLC, and there is only a $10 investment minimum on market orders. Alto’s CryptoIRA has a 1% annual fee, and a 1.5% transaction fee. As expected, Alto holds your hand for this process and helps simplify everything for you.

(Interestingly, creating a separate crypto product is done out of an abundance of caution. Alto’s CRO Tara Fung noted that regulators are just starting to look at whether tokens like Bitcoin should be held in retirement accounts. So when it comes to this brave new world, it’s best to pay it safe and keep the products separate.)

Alto and the “Checkbook IRA”

As we mentioned previously, some SDIRAs are “Checkbook LLCs,” and others aren’t. Alto offers both. However most folks take the easy route, and just open an Alto IRA or CryptoIRA and don’t add the Checkbook LLC. (Although it’s a bit more limiting, not having a separate LLC entity that you need to worry about makes things a lot simpler for everyone.)

We highly recommend checking out AltoIRA.

What are the risks of SDIRAs?

Even if AltoIRA abstracts away the difficulties with creating & managing an SDIRA, an IRA LLC comes with some knowledge requirements and the need for discipline with respect to how you conduct business. It’s important to understand the implications and risks.

- Prohibited transactions. If you break a rule, the entire account could be considered “self dealing,” meaning you’ll be on the hook for taxes and penalties.

- Due diligence. SDIRA custodians cannot offer financial advice. You’re on your own. The SEC notes that SDIRA custodians “don’t typically evaluate the quality or legitimacy of any investment in the self-directed IRA or its promoters.” This means you’ll need to do your homework and/or have a company help you. (Lucky for you this is exactly what we do here, with Alternative Assets Insider.)

- Fees. Alto’s fees are simple and straightforward. But other SDIRAs may have a complicated fee structure. Typical charges include account setup fees, annual fees, renewal fees, and fees for investment executions. These costs add up & cut into your earnings.

- Exit plan. It’s easy to sell stocks, bonds, and mutual funds: just place a sell order with your broker, and the market takes care of the rest. Not so with some SDIRA investments. If you own an apartment building, for example, it will take some time to find the right buyer. That can be especially problematic if you have a traditional SDIRA and need to start taking distributions.