You may have heard the classic maxim that the rich use “good debt” while the average person uses “bad debt.”

The idea behind the saying is that the rich borrow money to buy assets (like a home or a business). Everyone else, meanwhile, borrows money to finance consumer purchases (often with a credit card or personal loan).

But it actually goes even deeper than this.

Although the rich use debt differently than the average person, the ultra-wealthy also use debt differently than the “regular” rich.

When you get to stratospheric levels of wealth, you’re not just borrowing to buy a few more assets. Instead, you’re borrowing to:

- Drastically reduce your taxes

- Maintain control of corporations, and eventually

- Keep your fortune (mostly) intact as you pass it on to your heirs.

Today, we’re looking at the institutions and mechanisms that make this possible, and show you how private lending to the wealthy really works.

Providing banking services to the wealthy is a lucrative business – and has a history that’s influenced huge swaths of modern finance.

Let’s go 👇

Note: Most of this issue is free. But you’ll need the All-Access Pass to read the full thing.

Table of Contents

A short history of private banking

When modern finance emerged in the European Middle Ages, the most important financial regulator wasn’t a regulator at all — it was the Catholic Church.

While financial law was undeveloped at the time, religious law was all-encompassing. The Church, however, had a dim view of financial practice, even banning Christians from lending money to other Christians with interest (a sin known as usury).

(Note: This concept is not unique to Christianity! One of the key principles of Islamic Finance is that gains from interest are prohibited even today. To get around this law, companies use a workaround known as non-interest banking).

Back to Christianity. At first glance, the “no interest” rule might seem to bar early European Christians from starting banks, since there’s little point to do so without the profit incentive.

But in Lombardy (a region in North Italy), a few enterprising Christian bankers figured out a clever workaround to usury law:

- The Church has rules surrounding interest, but they had little to say about collateral.

- Instead of charging “borrowers” interest, we can buy the borrower’s assets upfront at (for example) $100.

- Then, we can enter into an agreement with the borrower for them to buy back their own asset one year later, for $105.

- After one year, we’ve earned $5 while the borrower got access to $100 in “credit.”

Voila, a 1-year 5% loan without charging interest!

You might recognize this as an early version of a repurchase agreement — a common tool in modern finance. (Less flatteringly, it also looks a bit like a pawnshop.)

But crucially, this collateral workaround fundamentally changed who could get credit. Since you needed assets to borrow cash, access to banking became the sole domain of the elite.

Despite being a resource-poor region, financial practices like this helped turn Northern Italy into an economic powerhouse during the Renaissance, with cities like Florence becoming some of the wealthiest in the world.

And while access to banking has become more egalitarian in the modern world, collateralized lending to the elite remains a core part of private banking — known, appropriately enough, as Lombard lending.

Lombard Loans in the modern world

Institutional memories of modern finance’s origins in Lombardy can be found all over the place, including Lombard facilities at central banks, and London’s famous Lombard Street.

But the most direct connection to the financial practices of North Italy in the Middle Ages can be found in modern Lombard loans.

What are Lombard loans?

There are two basic types of asset-based loans you can take out:

- A loan used to finance the initial purchase of an asset,

- Or a loan that’s collateralized by an already-owned asset.

A house, for instance, can be used to back a mortgage (type 1) or a home equity line of credit (type 2).

A Lombard loan is a type 2 loan that a bank extends to a wealthy client, backed by assets like property, stock, or even fine art. It lets the client unlock liquidity without needing to sell their underlying assets.

Banks lend up to a certain portion of the value of these assets, in what’s known as the loan-to-value ratio (LTV). For a Lombard loan, the LTV is typically set at 50% (though it can be lower for extremely illiquid/hard-to-value assets.)

Now, most “regular” clients can get access to a “quasi-Lombard loan” today (like a securities-backed line of credit, or the aforementioned HELOC).

But what makes Lombard loans special is their flexibility. Lombard loans are customized to the needs of the wealthy, including:

- Financing for niche assets, including sports teams and private jets (JPMorgan even has a yacht financing group)

- Flexible repayment terms, including no fixed repayment date and deferred cash interest (a crucial detail we’ll return to later)

- And, perhaps most importantly, generous interest rates, which are typically quite a bit lower than you can get outside these exclusive channels.

In recent years, Lombard loans have seen a resurgence among private bankers, on the back of an institutional push to promote these products.

But it’s not just for banks anymore. In the UK, a company called Sidekick has become the only UK-regulated provider to offer Lombard loans to regular clients as well.

The ultra-wealthy can not only access a wider variety of products, such as alternatives, but they also have the luxury of being able to lock their money up and benefit from the illiquidity premium.

Retail investors don’t have these benefits. They have to keep their money in cash (in anticipation of potential cashflow needs), or they invest and then become forced sellers when they need access to the funds, which significantly impacts returns.

Lombard lending can be a way to more comfortably put money to work, knowing you can access liquidity via a credit line if needed. The richest have known this secret for years, but in Europe this has largely not been made available to the wider retail investor base until now.

If this interests you and you live in Europe, let’s talk.

– Matt Ford, founder of Sidekick

Why Wall Street loves Lombard loans

As part of an increased focus on wealthy individuals in recent years, Wall Street banks have made Lombard loans a larger component of their strategy.

And sure, it’s not unusual for banks to lend people money – it’s quite literally their core purpose.

What is unusual is the amount of lending Wall Street banks are doing as part of their wealth management divisions.

See, historically, wealth management has been a fee-based business. Advisors made money by charging a ~1% annual fee on a client’s entire portfolio.

But lately, something called net interest margin (or the difference between what rate a bank can borrow and lend money at) has become an increasingly important revenue driver for wealth management departments.

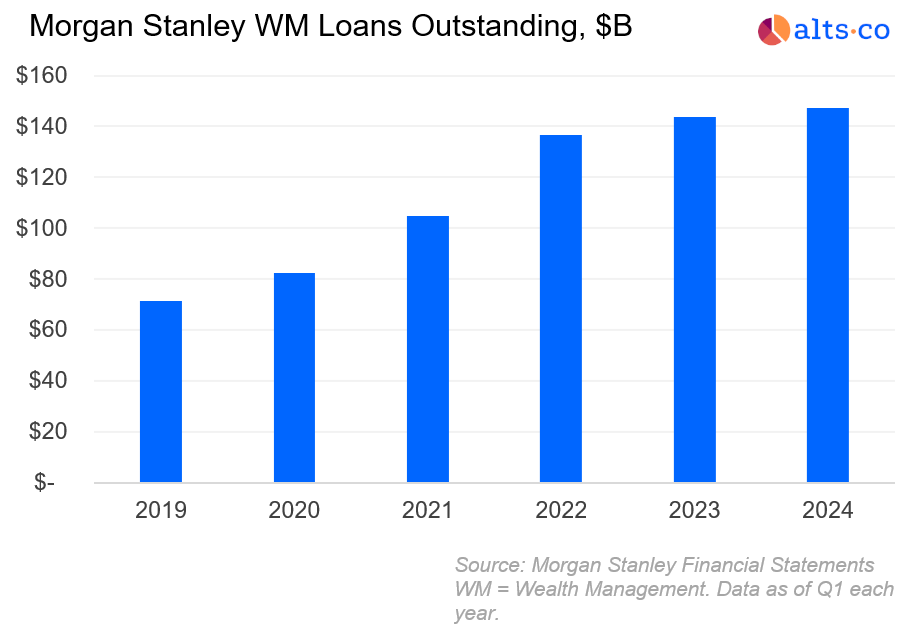

At Morgan Stanley, for example, lending by the firm’s wealth management division has more than doubled since 2019, growing from $71.5 billion to over $147 billion as of Q1 2024.

This approach is mirrored by competitors, including Goldman Sachs, who plans to double the amount of lending they do to clients worth at least $10 million in the next five years, from $33 billion today to $66 billion.

Meanwhile, Bank of America and JPMorgan both have wealth management loan books worth at least $200 billion.

And Wall Street doesn’t just love Lombard loans as an added fee driver. These loans can also help keep advisory fees in place.

If a client wants to withdraw a portion of their portfolio to make a big purchase, offering a Lombard loan can help retain those assets under management while still unlocking liquidity. This allows the bank to double-dip on the same assets (interest margin AND fees).

The increased popularity of Lombard lending is far from just a supply-side push. These loans are also a core tool in a sophisticated (and highly lucrative) tax avoidance strategy for wealthy clients.

The “Buy, Borrow, Die” strategy

This section discusses tax law, focusing specifically on the US. As always, we are not tax professionals and this is not tax advice!

First, we should note that there’s a big difference between tax avoidance and tax evasion:

- Tax evasion is illegal and will get you in a lot of trouble

- Tax avoidance, though, is the perfectly legal (but questionably fair) pastime of using the regulatory structure to minimize your tax bill.

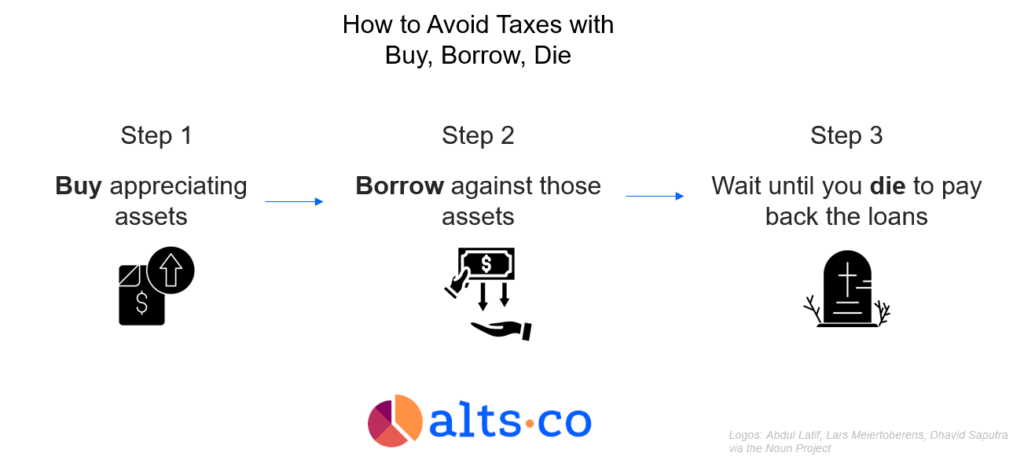

One of the most popular tax avoidance strategies among the ultra-wealthy (which appears to be currently used by the likes of Carl Icahn, Elon Musk, and Larry Ellison) is the infamous model of “buy, borrow, die.“

If you use it correctly, this model allows you to live off your wealth while paying little in taxes, all while passing your fortune to heirs as efficiently as possible.

What’s more, the generous flexibility of Lombard loans is a key part of making this strategy work…

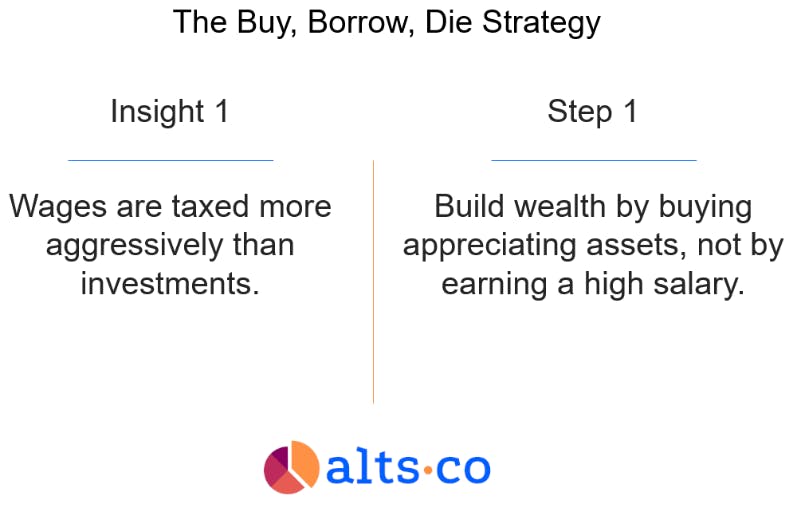

Step 1: Buy assets

In the US (and many other countries), wages are taxed far more aggressively than investments.

The highest long-term capital gains tax rate in the US is currently just 20% (compared with 37% for income).

Oh, and you can also claim tax benefits if you lose money on your investments, reducing the amount of tax you owe.

And while some investments do generate taxable income through dividends and interest, the multi-decade trend towards corporate buybacks has reduced this burden.

All in all, it’s far more tax-efficient to get rich by buying rising assets than through a high paycheck.

Better yet, you can start a high-growth company and pay yourself a de minimis salary while owning a huge swath of shares.

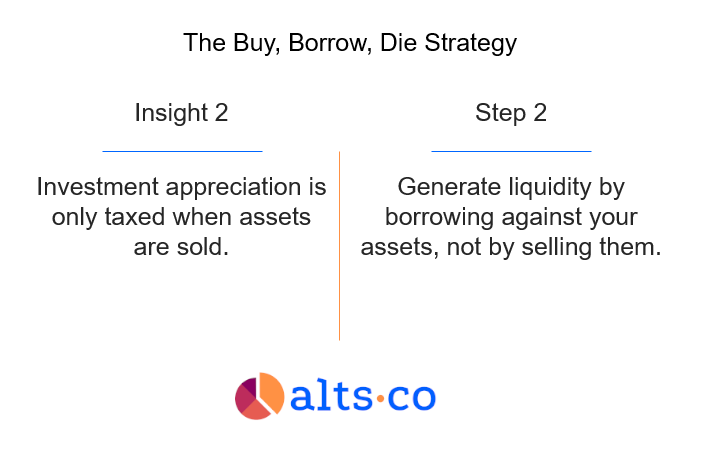

Step 2: Borrow instead of selling assets

But getting rich through assets poses a problem: this is paper wealth. You ultimately need cash to pay for things, right?

The second insight of buy, borrow, die is that you only trigger a taxable capital gains event when you realize asset appreciation by selling your assets. If you can keep those gains unrealized, you don’t owe a penny.

To extract cash from assets without selling them, all you need to do is borrow against them. Call your neighborhood private banker and negotiate a Lombard loan collateralized by your now-appreciated assets. (Or use Sidekick if you’re in Europe)

Plus, if you start a company, this trick lets you maintain the voting power of your stock while still enjoying a nice lifestyle (the ill-fated Silicon Valley Bank was a prime facilitator of this strategy for startup founders).

Step 3: Die (hey, it happens)

In theory, borrowing against your assets doesn’t remove your tax burden; it just delays it.

Eventually, you’ll need to sell those assets to repay your loan, at which point you’ll be subject to capital gains tax…right?

Not quite. So long as your loan-to-value ratio continues to be suitable, your Lombard banker will likely keep rolling over the loan as long as you need to, quite possibly up to the moment we die.

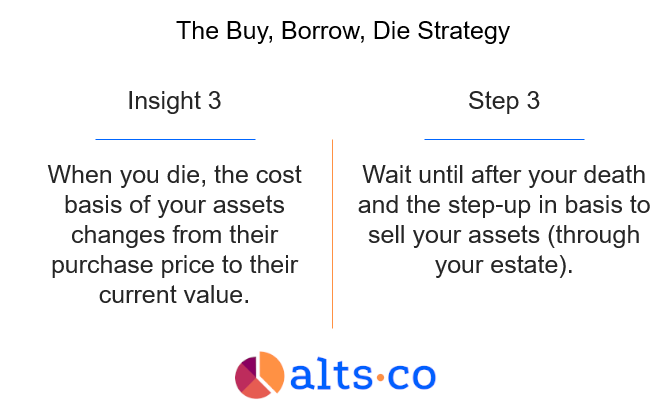

And as morbid as it sounds (hear me out) dying is a very tax-efficient move.

When assets are sold during your lifetime, they’re subject to capital gains tax on the difference between their sale price and their “basis” — usually the original purchase price.

When you pass away, however, your assets receive a step-up in basis.

This replaces the original purchase price with the asset’s market value at the moment of death. This means if your estate sells all your assets immediately after you die, it will owe no taxes on the transaction.

By waiting to sell your assets until after your death, you can pay zero capital gains taxes on a lifetime’s worth of appreciation.

Some of the sale proceeds will be used to repay the Lombard loan you’ve accumulated throughout your life. But the rest can be distributed to your heirs.

And with those three steps, you should be well on your way to enjoying your wealth and leaving a sizable legacy to your heirs — all without those pesky taxes to worry about.

Challenges and details

The idea of buy, borrow, die sounds great. But that’s just the start.

It’s critical to understand the practical challenges and important details, because they are ultimately what will make this strategy work for you. But you need the All-Access Pass for this section.

That’s all for today.

Reply to this email with comments. We read everything.

See you next time, Brian

Disclosures

- Neither the author, nor the ALTS 1 Fund, nor Altea has any holdings in any other companies mentioned in this issue.

- This issue contains no affiliate links.