Today we’ve got a short issue on investing in infrastructure. It’s an unsexy alt with a long track record of moderate & steady returns.

But we found some interesting stuff here. And we discovered a guy who values bridges for a living.

Let’s dig in 🔨

Table of Contents

How infrastructure is financed

When cities want to build new infrastructure projects (highways, bridges, schools, stadiums, etc) there are a few ways they raise money:

- Raise new taxes from citizens

- Raise new taxes from businesses

- Secure funding from state and federal governments (basically taxes that have been pre-earmarked)

- Issue debt through municipal bonds, or ‘munis’

- Create a Public/Private Partnership (called PPP or P3 arrangements)

PPPs are relatively new, and especially interesting. The new pedestrian bridge connecting Tennessee and Arkansas is a perfect example. Spanning over the mighty Mississippi river, the Big River Crossing was built using a design-bid-build contract, where the government put out a call for bids from private contractors. After proposals were evaluated, a contract was awarded to the lowest bidder.

Public/private projects are usually funded through a mix of federal grants, state funds, and funding from companies, sponsors, and philanthropists.

Not every public project goes smoothly. One famous example is The Big Dig in my childhood home of Boston, MA.

The Big Dig is something of a paradox. From a pure civil engineering standpoint, it was a triumph. 5,000 workers (including my old next-door neighbor) replaced this ugly-ass, crumbling, elevated freeway and put the whole system underground. They built a bunch of airport connectors, the cool-looking Zakim Bridge, and slapped a bunch of parkland on top.

But it also cost a shit-ton. What was projected to cost $2.6 billion (in 1982 dollars) will end up exceeding $24 billion, factoring in inflation and interest payments. It was (and still is) the most expensive public works project in US history, and some say that Boston should have done a private-public partnership instead.

Infrastructure as an asset class

Infrastructure has been a hot topic in the US since the passing of 2021’s $1 trillion infrastructure bill: The Infrastructure Investment and Jobs Act.

The bill is America’s largest infrastructure investment since Eisenhower’s interstate highway system (!) It intends to funnel hundreds of billions to state and local governments to improve or build highways, bridges, mass transit systems, and other good stuff. Its bipartisan passage sent a message about the importance of investing in the country’s crumbling infrastructure.

This money will flow into all sorts of projects. Some will be boring (filling cracks with tar snakes) others will be exciting (like California High-Speed Rail, which is actually happening).

Some projects will be fully taxpayer-funded, others will be PPP. Private-public projects have grown across the United States, where states and localities face looming infrastructure costs and shrinking public budgets.

Infrastructure investments allow corporations, private equity, and the public to get returns from investments in public developments & improvements.

What are the different types of infrastructure investing?

It’s more than just roads & bridges: Infrastructure projects include water & sewage systems, electric systems, communication systems, deep-sea cables, and more.

Over the last few decades, infrastructure investing has branched into four categories. In order of risk, they are Core, Core Plus, Value-Add, and Opportunistic.

Core

- Risk: Lowest

- Examples: Utilities, gas, electricity, water, waste, sewage. All the boring but totally necessary stuff. Can also include top-tier airports and seaports.

- Net IRR target: 6% – 9%

- Holding period: 7+ years

Core stuff never goes away. There is essentially no GDP or political risk. It’s considered the most stable form of infrastructure equity investing, because it’s the most essential to society.

Gains are basically all on the income side (there’s very limited upside through capital gains) and assets are commonly held for the long term.

This space is mostly all fixed-income investments with highly-regulated municipalities and top-tier industrial companies.

However, even this low-risk, low-return category may actually carry more risk than you’d think, particularly as entire fuel sources are getting phased out.

Core Plus

- Risk: Low

- Examples: Established oil & gas. Thermal power. Renewable power. Undersea cables.

- Net IRR target: 9% – 12%

- Holding period: 6+ years

Similar to Core, but with fewer monopolies. Some GDP and political risk here.

Think of this as core utility companies that have growth or expansion plans. For example, an oil company transitioning to renewable energy, or an airport adding a new terminal.

The holding period is generally a bit shorter, and returns are from both capital appreciation and ongoing income.

Value-Add

- Risk: Moderate

- Examples: Venture oil & gas. Toll roads. Fiber-optic cables. Data centers. Cemeteries.

- Net IRR target: 12% – 15%

- Holding period: 5 – 7 years

Value-Add is developing brand new infrastructure that approaches PE-like returns.

Think of it like Core Plus with a bit more risk and more upside from capital gains. Income is still a component of overall returns, but there is also scope for greater capital appreciation.

Interestingly, maturing legacy core industries combined with large-scale social changes (such as the acceptance of remote work), have moved some Value-Add assets down the risk spectrum (data centers) and others up the risk spectrum (toll roads).

Opportunistic

- Risk: High

- Examples: Power, water, oil & gas for developing nations

- Net IRR target: 15%+

- Holding period: 3 – 5 years

Opportunistic is building brand new systems from scratch for developing countries.

This is nation-building through Multi-National Development Banks (MDBs). It offers the best returns and lowest holding period — and most of the returns are from capital gains.

The problem with this stuff is that there’s significant GDP risk, social risk, political risk, and even currency risk. Assets are subject to a high degree of volumetric or commodity price exposure, and developing world politics means projects can be forced to stop on a dime.

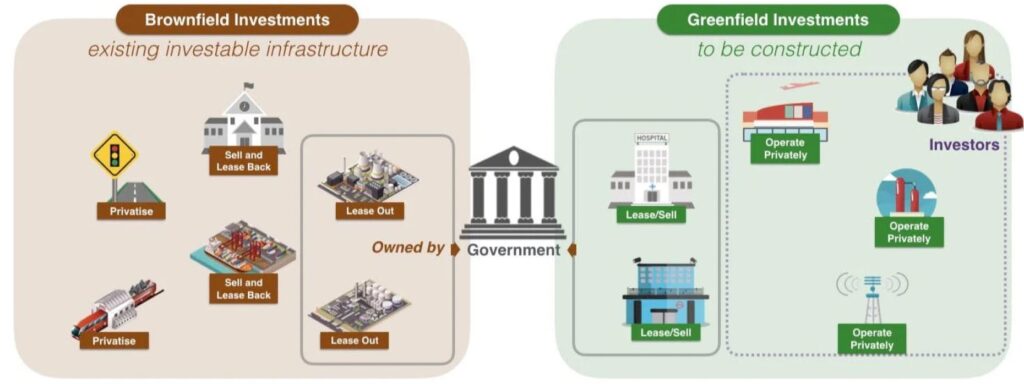

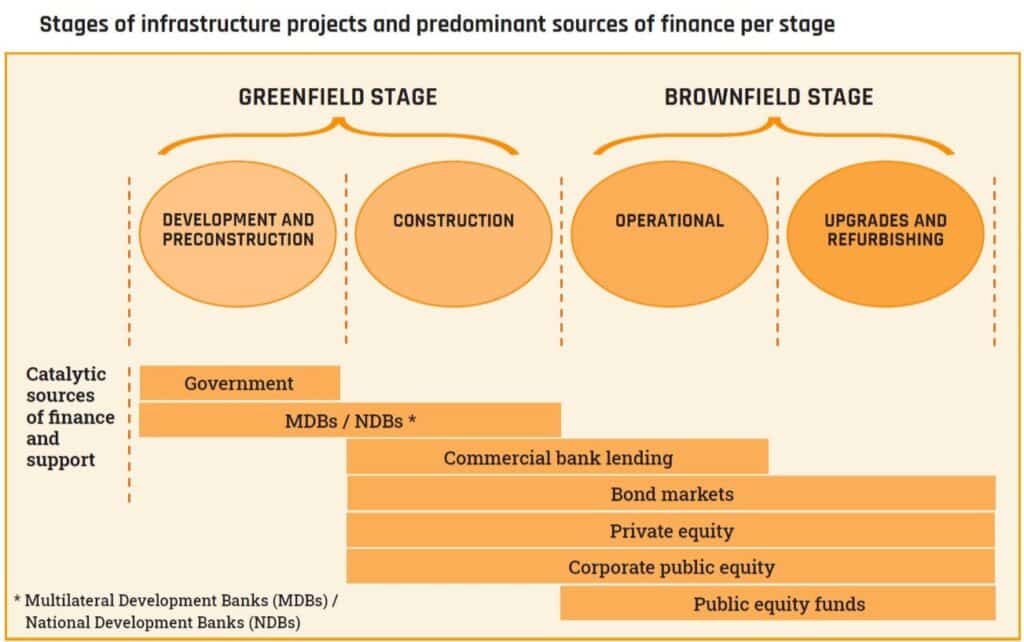

Greenfield vs brownfield investments

When talking about infrastructure, you’ll often hear about “brownfield” and “greenfield” investments.

These describe the stages in which projects begin:

- Brownfield investments are pre-existing. This is when a company takes over a pre-existing asset through a lease or a buyout, with the intention of fixing it up. These investments are de-risked. As the asset matures, investors can re-sell the facility at an appreciated value, making them common in Core Plus.

- Greenfield investments are yet to be constructed. These projects begin from scratch. For example, a government contract for a new electric facility (a greenfield investment) can provide steady cash flows for investors because governments are relatively stable and predictable.

How to invest in infrastructure

This is much different than buying baseball cards.

Investing in infrastructure requires a vast amount of capital (minimum ticket size is usually around $200 million) which is why PE and managed funds like it so much.

Due to the large capital outlay required, unlisted infrastructure has generally been very hard for many institutional investors to access. But companies like iCapital are opening up fund access to tens of thousands of wealth managers, RIAs, and financial planners.

To put it another way, infrastructure is being “fractionalized and democratized” for institutional investors, but not yet for retail investors.

Private Equity funds

As you recall, many investment opportunities arise out of public-private partnerships. But these projects are often made possible because of PE’s unique ability to raise money and “connect the dots” between parties. It’s a connections game. Someone’s gotta lead the charge, and PE is in the optimal spot here.

In a private infrastructure equity fund, an investor takes part ownership of the infrastructure company. A rise in the company share price increases the value of the entity that has invested in the infrastructure equity fund.

Equity investors also share in the dividends paid by the company. There’s no guaranteed return like debt investors get, but the returns aren’t capped. And when a company is very profitable, the returns can be quite good.

Private debt funds

Private infrastructure debt funds are like income funds for accredited investors. They focus on established, brownfield investments that provide essential public services and benefit from stable and predictable cash flows.

Infrastructure projects tend to be good candidates for debt financing arrangements because of the generally stable and dependable cash flows — and it’s less risky than equity investing too. If the project doesn’t make money, the interest payments take priority. The debt investors still get paid.

The infrastructure debt market has changed quite a bit in recent years; markets are more open than ever. Many institutional investors are considering allocations to infrastructure debt, attracted to the industry’s potential for long-term cash flows, diversification, and attractive risk-adjusted returns.

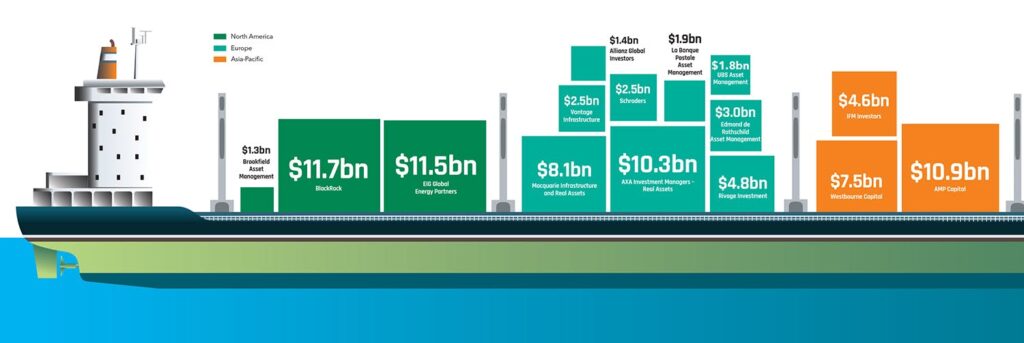

In 2021, private debt funds raised $193.4 billion, a 14% jump from 2020. The most active private equity investors in the last five years include BlackRock, AMP Capital, Blackstone, The Carlyle Group, and Canadian-based Caisse de dépôt et placement du Québec.

Public infrastructure funds

Infrastructure funds are publicly-traded mutual funds and ETFs tailored toward public assets and services that people depend on daily.

You can invest in an infrastructure fund by buying shares via an online brokerage account. Or you can check your IRA or 401(k) fund options to see if infrastructure funds or ETFs are included.

Notable funds include:

- Global X US Infrastructure Dev ETF (PAVE) is up 60% over 5y

- Lazard Global Listed Infrastructure Port (GLIFX) is flat but offers a nice 5.5% yield

Infrastructure funds usually include municipal bonds, but investors can also just buy these directly.

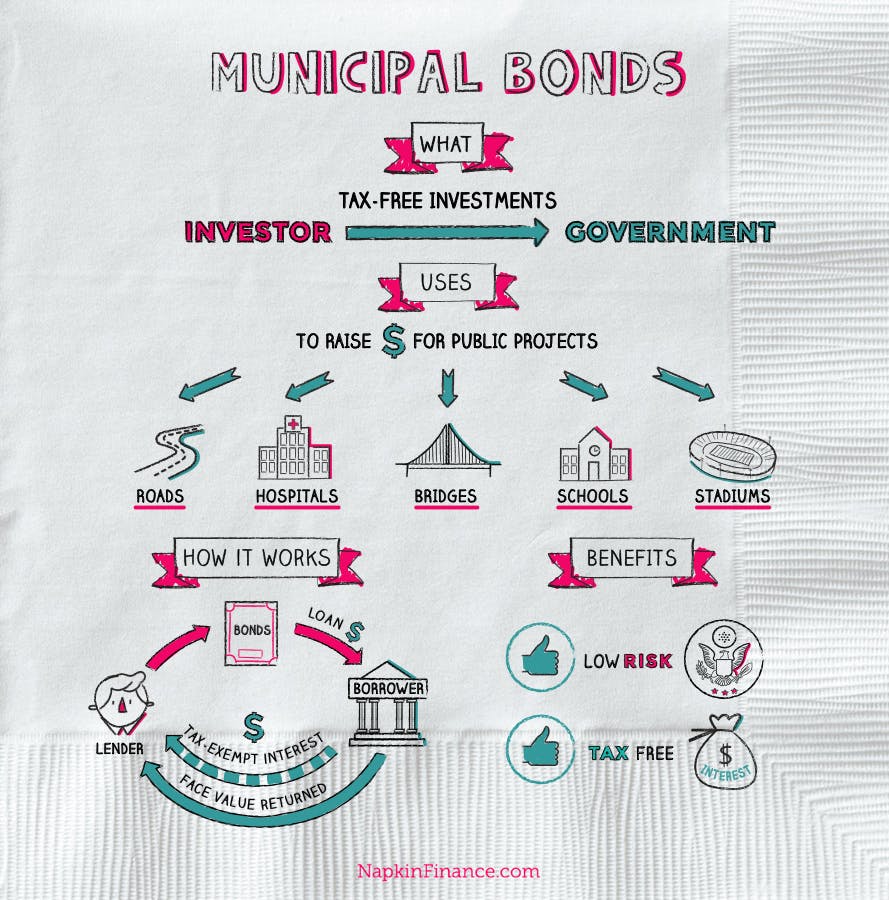

Municipal bonds (munis)

Munis are basically loans that investors make to local governments to fund hospitals, schools, stadiums, etc.

Investing in munis is boring, but comes with a big tax advantage. Munis only pay a few points in interest (2-4%). But unlike corporate bonds, the interest paid is tax-free, making them an attractive safe option for folks in high tax brackets.

- General obligation (GO) munis provide cash flows generated from taxes collected on a project.

- Revenue munis return cash flows generated from the project itself.

How public infrastructure is valued

In researching this topic, we discovered an interesting character.

Let’s say you’re a city with a huge piece of infrastructure in need of repair. Perhaps a bridge that needs upgrading, or an airport that needs a new terminal. Before you can begin work, you need to assess the asset’s value, so investors understand the starting point and funding can be secured.

But how would you even begin to value something like a bridge, a highway, or a seaport? Enter the public infrastructure appraiser.

Appraisers play a crucial role in determining the values of famous landmarks and everyday infrastructure critical to a city’s economic activity.

One of the most well-known appraisers is Bharat Kanodia. Bharat has estimated the values of some of the world’s largest and most structures, including the Golden Gate Bridge, the Eiffel Tower, the Brooklyn Bridge, and the Hartsfield-Jackson Atlanta International Airport.

In his methodology, Kanodia accounts for building costs at present-day value, labor costs, impacts on tourism, and an asset’s economic impact on all industries.

Appraisals are also done for insurance purposes. There are insurance companies that cover infrastructure for cities, including natural disasters, terrorism insurance coverage, and breaks resulting from natural wear & tear.

According to Kanodia, rebuilding the Eiffel Tower would cost about $2.25 billion. The What It’s Worth YouTube channel does some great breakdowns on stuff like this.

Advantages of investing in infrastructure

There are some distinct advantages to investing in infrastructure:

- Inflation hedge. Assets are tied to inflation markers that give investors protection from inflationary pressures

- Tangible asset that retains value even in economic downturns

- Cash flows (dividends) are more predictable and less correlated to public & private markets

- Resiliency. Hard assets are more resilient and dependable forms of investment, built for long-term conditions.

- High barriers to entry can inhibit competition and lead to investments in monopolistic or semi-monopolistic industries.

New technologies mean that new infrastructure is in development every day and is churned out in various phases over a set of years. Investors looking to capitalize on innovations could do well by finding investment opportunities that address new forms of infrastructure.

Closing thoughts

Aside from farmland and agriculture, infrastructure is basically the most important thing in the world.

This asset class has traditionally been a boring, conservative alternative investment. And it can definitely be a bit stodgy. This stuff doesn’t go to the moon.

But over the past 10 years, the asset class has been shaken up by a slew of technological revolutions. Green energy. Mobility. Desalination. EV charging networks. Battery storage. Hydrogen distribution. 5G. Data centers. Smart motorways. Smart rail.

Suddenly there are new types of infrastructure investments presenting unique opportunities for investors. It’ll never be sexy, but it’s what powers society forward, and can have big tax benefits.

I think the future lies in private-public partnerships; companies like Transurban that don’t just design, bid, and build infrastructure, but operate it as well.

Investing in infrastructure means playing the long game, and the private deals are still out of reach for non-accredited investors. But if you want stable growth backed by monopolistic supply, inflation-resistant stability, and don’t mind a long commitment, then infra’s for you. 🏗️

Disclosures

- None of the authors have direct financial interests in any assets or investment opportunities mentioned in this issue.

- None of the assets or investment opportunities mentioned in this issue are held in our ALTS 1 Fund.

- This issue is loaded with affiliate links to many different companies (though Discogs isn’t one of them — Stefan just loves that site.) Anyways, we may collect a share of sales or other compensation if you purchase something through these links,