Today, Brian Flaherty teamed up with crypto expert John Belitsky to demystify one of the most practical, yet least-understood use cases for blockchain technology: tokenization.

In this issue, Brian and John explain:

- How does tokenization work?

- Does it actually offer anything new?

- What problems does tokenization solve?

- What shortcomings does it have?

- What projects can you invest in to ride the wave?

If this stuff confuses you, read this issue. It’ll clear things up.

Already well-versed? You’ll still learn plenty.

Let’s go 👇

Table of Contents

It’s time to take tokenization seriously

Looking at the crypto market right now, we’re getting a strange sense of déjà vu.

The winter has thawed, prices are up again, and suddenly we find ourselves in times reminiscent of 2020’s bull market run.

Bitcoin and Ethereum are flirting with and exceeding all-time highs, contributing to spikes in meme coins like Shiba Inu, Dogecoin, and many others I won’t bother naming.

As crypto once again starts to command the headlines, some old buzzwords are making a resurgence — including tokenization.

Tokenization was all the rage in days gone by, when it seemed like every company was “pivoting to the blockchain.”

High-profile projects

For the most part, corporate tokenization efforts have largely fizzled out. It’s tough to point to any significant, lastingchanges the first wave of tokenization brought to financial markets.

This time around, though, things seem different.

For one thing, major banks and institutions are now getting involved. For another, they’re launching genuinely functional projects, not just putting out press releases:

Digital bonds

Lately there has been strong growth in digital bonds (aka tokenized debt on the blockchain), with issuance from banks like UBS and SocGen and the governments of Colombia and Hong Kong.

New payment rails

Last November, JPMorgan launched its blockchain-based Onyx platform, including adding programmable treasury features for corporate clients. They are already doing billions in daily transactions.

Meanwhile, Citi successfully completed a proof-of-concept test for private market tokenization last month.

Tokenized funds

Just four days ago, BlackRock, one of the largest asset managers in the world, launched a tokenized fund with (and made a big investment in) tokenization firm Securitize.

And just a few weeks ago, a group of banks, including Goldman Sachs and BNY Mellon, completed a series of test transactions on a regulatory-compliant interbank blockchain called “Canton.”

Given the number of high-profile projects from big players, it’s safe to say we should be taking the current tokenization push seriously.

But unless you’re knee-deep in the crypto space, the concept of tokenization probably confuses you.

Let’s take a step back and explore what tokenization is all about — and why it’s fundamentally distinct from existing practices.

What is tokenization?

Issuing digital records of a real thing

At its core, tokenization is about creating digital assets on a blockchain.

Think of a blockchain as a gigantic, publicly viewable database that anyone can write to (kept secure by mechanisms like proof of stake or proof of work).

This database basically includes a record of every single account and digital asset on the chain, as well as all transfers between accounts.

In a nutshell, tokenization is just issuing digital records of a real thing.

Complete vs incomplete tokenization

In researching this topic, I found it helpful to view tokenization as a spectrum, with complete, or “pure” tokenization on one end and incomplete tokenization on the other.

Pure tokenization is where the actual asset lives on the blockchain, rather than just a representation of that asset.

On-chain NFTs are a perfect example. The entirety of what’s owned is just data stored on the blockchain — like an image or a text file.

But pure tokenization isn’t always the best solution. Even simple digital objects can require huge amounts of data to describe them, making storing and transacting those tokens challenging.

And, in fact, if we ever want to digitize traditional financial assets (which live on exchanges) or real-world assets (which live, you know, in the real world), then we’ll need to sacrifice the idea of pure tokenization.

So, the “next best option” is the complete digital representation of an off-chain asset.

As a practical example, consider tokenizing a corporate bond, which can have many features including par value, maturity term, interest rate, preference in the capital stack, etc.

The more you can represent those features as data points stored on the blockchain (and updated through off-chain data sources), the more truly “tokenized” the bond is.

The less information included, the less complete the digital representation is — and the worse the tokenization.

And here’s why tokenization matters: once you’ve built a token to serve as a digital representation of an asset, it’s just a small leap to fractionalizing, trading, and pricing that token — arguably with superior liquidity than the underlying, untokenized asset could ever have.

How does tokenization differ from existing practices?

The idea of digitizing and fractionalizing assets to increase liquidity and “democratize” ownership (sorry, I know everyone hates that term) isn’t new.

In fact, this is one of the biggest financial megatrends over the past decade, as evidenced by the rise of companies like EquityMultiple (real estate) Masterworks (art), and a slew of other companies we probably have affiliate links for.

Although unlocking access to investments previously out of reach for average joes is part of what tokenization offers, it’s a mistake to think there’s nothing new here.

Being on the blockchain comes with some unique benefits:

Benefit 1: You get a built-in exchange

If you’re trying to start a marketplace to invest in and trade shares of fractionalized investments, there are two big hurdles: technology and trust.

You need to a) build the technology, and b) get people to trust you enough to deposit funds.

But if you create a token on say, Ethereum*, you immediately jump over both hurdles.

* Note: Ethereum isn’t always a terrific solution, given a) the transaction costs, b) the fact that it’s a public ledger, and c) it doesn’t allow for a meaningful description of the asset, since metadata can’t be stored on the Ethereum network itself. But I digress…

The point is that the underlying trading and custody technology is already there, you just need to iterate on top of it.

Oh, and people already hold $100+ billion on the chain, which they can easily direct toward your project, with the Ethereum token itself having a market cap of $400B+.

Benefit 2: You get smart contracts

Think of smart contracts as programmable financial transactions.

For example, a smart contract might act as an escrow contract between two parties; automatically releasing funds once certain conditions have been met.

More complicated projects include things like Tune.FM, which aims to pay artists musical royalties as their songs are streamed (in real time!) through its JAM token.

Smart contracts have also created the possibility of entirely new types of financial instruments, including flash loans — instantaneous, collateral-free, and interest-free lending to help exploit arbitrage opportunities.

Benefit 3: You get a leaner financial system

Finally, tokenization could lead us toward a more efficient and transparent financial system built on the blockchain.

Right now, financial counterparties “speak” to each other using a web of different languages, including email, Excel spreadsheets, API connections, phone calls, even fax (yup, that still exists).

But if all of the counterparties are on the same “chain,” everyone can speak the same language, creating the possibility of a truly interoperable financial system.

Now, this standardization already exists in some pockets of the financial system. (One great example we’ve highlighted is the interbank networks that link ATM machines.)

But the blockchain creates a network that could link the entire system. A network of networks.

What are tokenization’s pitfalls?

A world where assets have their own digital counterpart sounds great in theory.

But is it practical?

Problem 1: Ownership is a legal gray area

Okay, you may have noticed we’ve been imprecise on the exact connection between digital tokens and the assets they represent.

There’s a good reason: this is a very complicated legal gray area. The extent to which ownership of an asset’s digital token, legally corresponds to ownership of the asset itself, is uncertain.

In the real world, you can prove ownership of major assets through things like contracts, deeds, and titles (For example, if you sell your car, the most critical step is signing over the vehicle’s title to the new owner).

But at the end of the day, the only reason these documents are “proof,” is because a court is willing to rely on them to enforce ownership.

For example, let’s say you bought an NFT that claims to represent ownership of a real-world asset without another form of property documentation — like an expensive watch.

If you buy the NFT, but the seller refuses to actually give you the watch, would a court enforce your ownership of the property? Is the NFT purchase as good as a signed contract? Who knows! Good luck buddy!

And these ownership questions get even more complicated when you consider tokens that fractionalize an asset among thousands of investors.

Regulation is coming…

In Wyoming, DAOs (decentralized autonomous organizations, a mechanism for pooling investor funds for tokenization efforts) were recognized as legal companies in 2021.

Wyoming is also attempting to make its own stable token, which will trade 1-for-1 with the US dollar. Legislation is passing before our eyes.

But overall, regulation is slow-moving, and not always consistent between jurisdictions.

Problem 2: Tokens might be securities

Questions over property rights are just the beginning.

Another challenge involves whether or not tokens qualify as securities (be it under current US law, or the law of other countries, etc).

Securities are governed by a set of rules which restrict their sale and secondary-market trading. In the US, this is all enforced by the Securities and Exchange Commission, so figuring out whether a token you want to create is a security or not is pretty important.

In the US, whether or not something is a security is determined by the “Howey Test.”

The test states that, in order to be a security, it must satisfy four criteria:

- An investment of money

- ..in a common enterprise

- ..with the expectation of profit

- ..derived from the efforts of others.

Based on the Howey Test, a cryptocurrency like Bitcoin is not a security (the SEC has clarified that criteria #3 and #4 are not satisfied — Bitcoin isn’t issued to raise capital for a company like a stock or bond.

But for digital tokens more generally, the situation isn’t clear.

For example, last year a judge found that Ripple (XRP), a token mostly designed as a payment mechanism, can sometimes be a security, depending on whether you’re selling it to retail or institutional investors.

As another example, consider an NFT which represents ownership of an entire house.

This probably isn’t a security, since buying a house definitely isn’t one.

But if you divide that NFT into 1,000 tokens and sell those, perhaps it becomes one indeed.

Right now, the SEC is suing Coinbase for acting as an unregulated securities exchange, on the theory that most digital tokens are, in fact securities.

For better or for worse, the case should provide some important clarification and precedent for these issues.

Problem 3: Transparency is a mixed bag

Many of the benefits of tokenization come from the fact that tokens run on a blockchain.

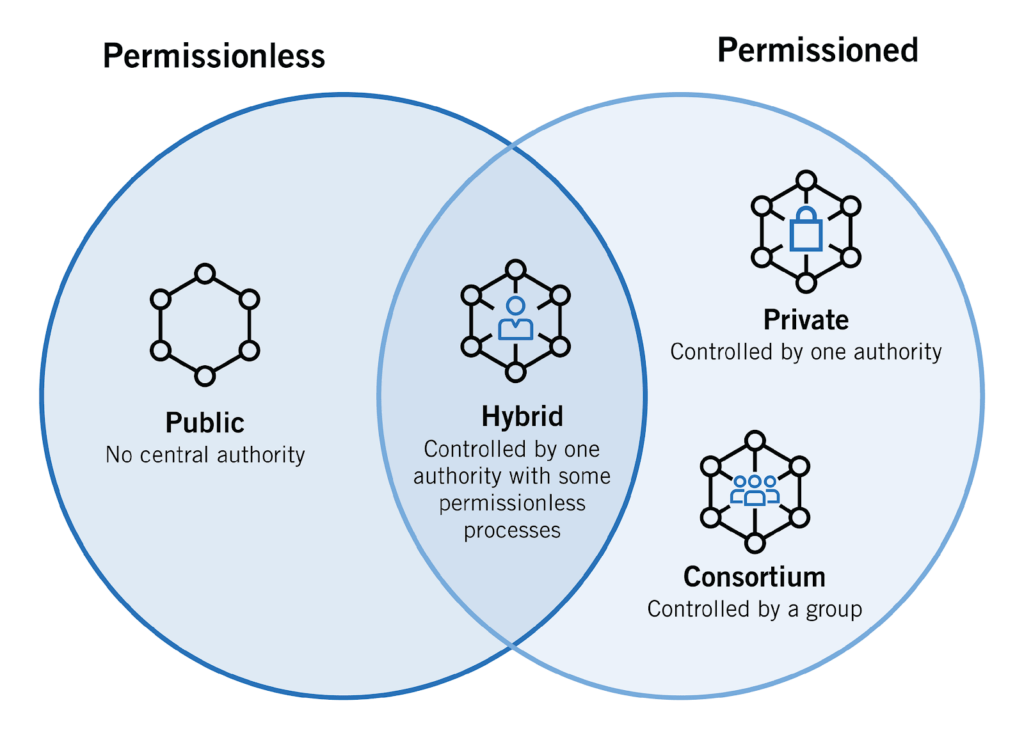

Throughout the piece, we’ve used the working definition of a publicly viewable, writable, and verifiable database to describe a blockchain. But this actually just describes a public blockchain (like Ethereum).

You can also make a private blockchain (effectively just a private database), where a single party can edit and control access.

Between these live a mix of semi-private, semi-public, and permissioned blockchains in which multiple parties run the network, determining who’s allowed in and how the system works.

Tokenization purists might say that only a public blockchain can create the transparency needed to facilitate an efficient and democratized financial system.

But here’s the thing: total transparency isn’t automatically a net positive for everyone!

Hedge funds frequently seek to hide their stock positions through derivatives to conceal their current trading strategies.

Wealthy people have nothing to gain (and plenty to lose) by blasting all their transactions to the world.

And the fact that transactions are publicly viewable means that account holders can often be identified based on their activity — even for wallets that are supposed to be anonymous.

Ask yourself:

- Would you be comfortable in a fully tokenized world, where all your investments are held on a public blockchain?

- Would you be comfortable with the risk of your account being linked to your identity?

- Would you be okay with everyone being able to see exactly what you own?

All this is to say that a tokenized future may not be built on transparent public blockchain. And that would mean interoperability and investor access would suffer.

What tokenized investments are available now?

I think tokenization has value as a structured, repeatable mechanism for taking previously uninvestable assets (especially in alternatives!) and turning them into liquid investments.

For the practice to really take off, though, I also think there needs to be substantially more regulatory clarity over the ownership rights afforded by digital assets and their status as securities.

If you want to dip your toes into tokenized investing, here are some projects worth exploring.

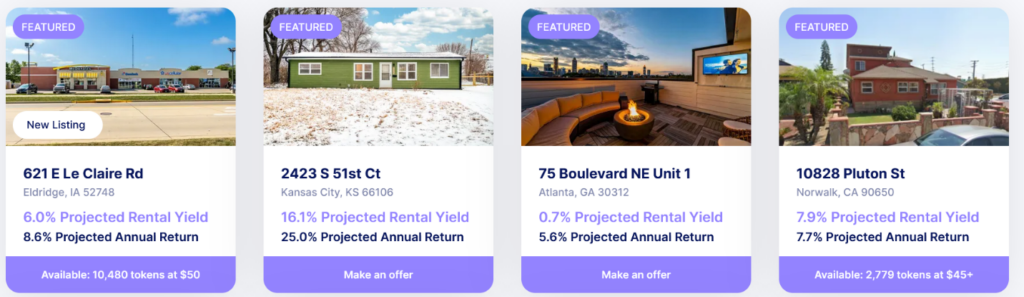

Real estate

Real estate is arguably the most logical use case for tokenization. It’s certainly one of the fastest-growing areas.

- Lofty, which offers its own tokenized real estate investments.

- Honeybricks, whose smart polygon contracts provide a legal wrapping that allows them to be represented by cryptographic digital securities

- Vave, which offers individual tokenized real estate investments as well as a bundled REIT token.

- RealT, which tokenized its first property in June 2019, and was the first Tokenized Real Estate Lending platform in the world with a market of $5 million.

Private debt & private equity

The high returns and inaccessibility of private equity & debt make them a prime target for tokenization:

- Goldfinch focuses on lending stablecoins to real-world businesses, with a current active loan value of nearly $100M.

- Obligate, which also does private credit lending, recently launched its first tokenized structured investment product.

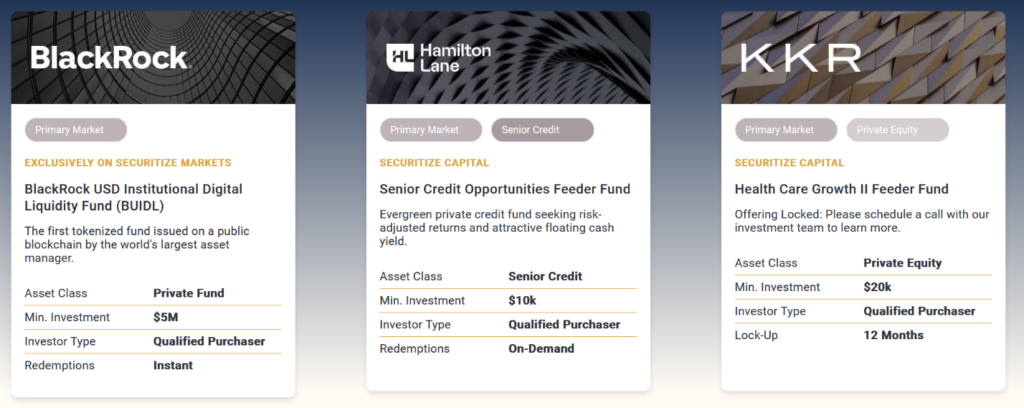

- Finally, Securitize is a big player in this space, offering access to tokenized funds from leading players in traditional finance like KKR and Hamilton Lane. (They also just struck a deal with Blackrock)

Precious metals and commodities

Tokenization efforts for commodities and metals are particularly interesting because traditional finance sometimes only offers exposure to such assets through future contracts:

- Pax Gold offers a digital token backed by physical gold stored in London.

- PermianChain is a platform tokenizing “confirmed deposits of natural resources” – including oil and gas.

- Finally, a project backed by Visa named Agrotoken launched late last year with the aim of issuing tokens backed by agricultural commodities including soybeans and wheat.

That’s all for today. A big thanks to John Belitsky for advising on this issue.

Reply with comments. We read everything.

See you next time,

Brian

Disclosures

- This issue was sponsored by MoonPay

- The co-author and the ALTS 1 Fund has multiple crypto holdings, including BTC and ETH.

- This issue contains affiliate links to Lofty, Honeybricks, Masterworks, and Equity Mulitple.